February 25, 2015

Existing Single Family Sales Go Up at End of Year. Mortgage Purchases Increasing.

- December 2014 existing single family sales ten percent higher than December 2013

- Overall sales were less in 2014 than 2013, but trending upward

- Watch listings: 2014 new monthly listings less than 2013

- Median sale price in December highest month in 2014

- Sale Volume $160,000,000 higher in December 2014 than December 2013

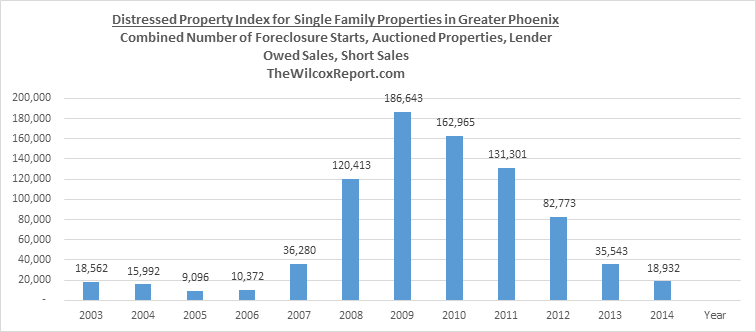

- 2014 Distressed Property Index lowest since 2006

- 2014 cash purchases lowest since 2008

- More purchases with a mortgage in 2014 than 2013

- Grand Canyon Title acquired by Fortune 500 Company. See page two.

- Big changes coming to residential real estate closing process starting on August 1, 2015. See page seven.

This report covers existing single family property sales in Greater Phoenix. Greater Phoenix is defined as Maricopa County. The data in this report, unless otherwise mentioned, is from the Arizona Regional Multiple Listing Services, Inc., also known as ARMLS.

In this report we compare performance for sales, sales volume, cash purchases, mortgage purchases, and new monthly listings. The report includes the Distressed Property Index covering foreclosure starts, auctioned properties, lender owned sales and short sales for the last twelve years. Most of the comparisons are year-over-year, comparing a time period in 2014 to the same time period in 2013. Year-over-year comparisons are an effective way to measure performance, highlight differences, and negates the effect of seasonality.

![]()

On January 1, 2015 Grand Canyon Title Agency was acquired by a Fortune 500 company. Grand Canyon Title became a division of Fidelity National Title Agency (FNTA). FNTA is a subsidiary of Fidelity National Financial (FNF). FNF is ranked 316 on the Fortune 500.

http://fortune.com/fortune500/fidelity-national-financial-inc-316/

FNF has more claim reserves than any other company in the industry. With more than a billion dollars in claim reserves to protect you, contact me to open your next commercial real estate transaction.

http://fidelitydfw.com/page/Financial-Strength.aspx

Existing Single Family Sales and Sale Volume

Sales were dismal for much of 2014. There were 6,563 less existing single family sales in the first three quarters of 2014 compared to 2013. Then the course reversed. In December 2014, there were 420 or ten percent more sales and $160,000,000 more in sale volume than in December 2013. These numbers made December 2014, on a year-to-year basis, the best month of 2014. Sale volume in the first eight months of 2014 was less than for the same months in 2013.

Not only were December 2014 existing sales higher than December 2013, but so were purchases with conventional, FHA and VA loans!

Distressed Property Index

Disappearing cheap distressed property for sale was a reason for less sales in 2014. According to the Arizona Regional Multiple Listing Services, Inc. (ARMLS), there were 2,149 less lender owned sales and 4,934 less short sales in 2014 compared to 2013. The Distressed Property Index in 2009 was 186,643 compared to 18,932 in 2014 for a decrease of 90%. However, the disappearance of cheap sales diminished cash sales. Cash sales were less every month in 2014 compared to 2013, resulting in 7,370 less cash purchases in 2014. Cash sales in 2014 were the lowest since 2008.

Sales under $50,000

Gone are the days when there were thousands of sales under $50,000. In 2014, there were 207 existing single family sales under $50,000 compared to 625 in 2014. From 2009 through 2013 there were 22,513 sales under $50,000. So the good news is that the glut of cheap distressed properties for sale that previously drove down home values are gone.

6,154 more sales in 2013 than 2014

7,368 more cash sales in 2013 than 2014

1,214 more sales with a mortgage in 2014 than 2013

On August 1, 2015 new rules apply to residential real estate closings.

Do you know what they are?

On August 1, 2015 new rules apply to most closed-end consumer mortgages. The rules effect existing and new home purchases, refinances, loans secured by vacant land, construction only loans, and timeshare loans. Excluded are reverse mortgages, home equity lines of credit, mortgages secured by a mobile home or a dwelling that is not attached to real property.

The Consumer Financial Protection Bureau or the CFPB a creation of the Dodd-Frank Act, has integrated mortgage disclosures and created new forms. For loans originated on August 1, 2015 or later, the Good Faith Estimate and the Truth in Lending will be replaced with a new document called the Loan Estimate. And the final Truth in Lending and Settlement Statement are replaced with a new document called the Closing Disclosure.

How will this affect the closing of real estate transactions? The timing of workflow and closings will be impacted by the new rules. The Closing Disclosure has new time tables associated with it. There is a Delivery Period and a Waiting Period before the borrower is allowed to sign loan documents.

Ken Trepeta, Government Affairs for the National Association of REALTORS suggests adding fifteen more days to the normal closing process time in this video.

http://www.realtor.org/videos/hud-1-going-away-understand-new-closing-forms-procedures

There is much more to the upcoming changes, for more detailed information contact me, Fletcher Wilcox, at FWilcox@gcta.com or 602.648.1230. I will be representing Grand Canyon Title Agency in meeting with real estate designated brokers and their agents, and builders, and banks and lenders and their loan officers. Don’t wait to learn about the changes, but find out what you need to know, what you need to do, and how the changes impact your clients.

Number of Buyers Purchasing with a Loan Improves. Fourth Quarter 2014 Best Quarter Year-To-Year

Purchases with a mortgage were 4.7% less in the first quarter of 2014 compared to the first quarter of 2013. As the year went on mortgage purchases gained momentum. In 2014, mortgage purchases up 1.3% in the second quarter, up 5.8% in the third quarter, and up 9.5% in the fourth quarter compared to the same quarters in 2013. However, the increase in mortgage purchases in the second and third quarters of 2014 was not enough to overcome the decrease in cash purchases resulting in less sales.

Segmenting Mortgages into Three Categories: Conventional, FHA and VA Loans

When segmenting mortgage purchases by conventional loans, FHA loans, and VA loans, we find the following results: Year-to-year conventional loan purchases were down the first three quarters in 2014 compared to 2013. A likely, partial reason for the decrease in conventional loans was the implementation of the new Dodd-Frank mortgage rules effective on January 10, 2014.

FHA loans were less only in the first quarter of 2014 compared to 2013, and VA loans were a hero all year long in 2014, up ever quarter of 2014 over 2013.

Keep Your Eye on Listing Inventory

The chart below is for new monthly listings of existing single properties in Greater Phoenix. The chart does not represent the total number of existing single family listings, but only new monthly listings. New monthly listings in 2014 were less from June through December compared to 2013.

Fletcher R. Wilcox

Fwilcox@GCTA.com 602.648.1230

Author of TheWilcoxReport.com(TM)

![]()

Follow Fletcher