I want to invite you to a class I am teaching on the changes to the real estate closing process that will take effect in about two months, this August 1, 2015. These changes will affect your buyers and sellers. This class is approved by the Arizona Department of Real Estate for three hours of contract law.

Some of the topics we will discuss are what your buyers and sellers should know about the new closing process. How the new closing process will influence contract writing. We will use scenarios. We will discuss why did a representative from the National Association of REALTORS say that real estate agents may want to add fifteen days to the close of escrow. What your sellers and buyers needs to know about the title insurance, the Closing Disclosure and AAR Residential Resale Real Estate Purchase Contract. Did you know a new contract is coming out this summer. What might change?

This Friday, May 29, from 9:00 a.m. to 12:00p.m. the Scottsdale Area Association of REALTORs (SAAR) is hosting the class CFPB – The “NEW” Loan Estimate & Closing Disclosure Forms. The class will be held at SAARs new state of the art facility located at 8600 East Anderson Dr., Suite 200, Scottsdale, AZ 85255 • Phone (480) 945-2651 Click the link below to sign up.

Some terminology you will need to know

- The Closing Disclosure

- The Delivery Period

- The Waiting Period

- Business days versus calendar days

- Consummation

- Why the amount of the owner’s title insurance policy and the lender’s title insurance policy shown on the Closing Disclosure may be different than what the buyer and seller actually pay

Click the link below to sign up. The cost is twenty dollars.

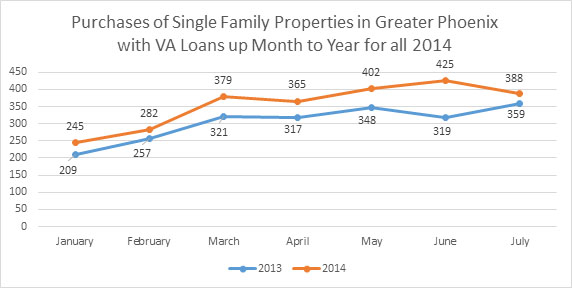

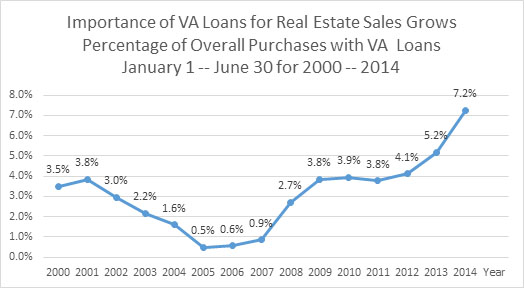

And there will be a short review of residential sales trends, such as how the number of single family homes being purchased with conventional loans, FHA loans, and VA loans are increasing. I will answer why they are increasing.

I hope to see you next Friday.

Fletcher R. Wilcox

CFPB External Operations Expert

V.P. Business Development

Real Estate Analyst

Grand Canyon Title Agency

Grand Canyon Title Agency is a wholly owned subsidiary of Fidelity National Financial (FNF). FNF is ranked number 316 on the list of Fortune 500 companies.

Follow Fletcher